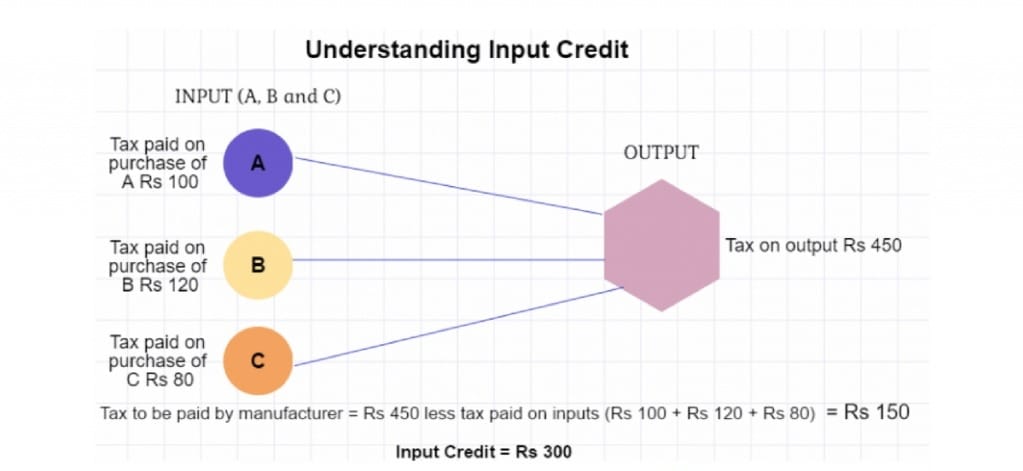

Input Tax Credit (ITC) is a mechanism in the taxation system that allows businesses to offset taxes paid on inputs against taxes they owe on outputs. It ensures that taxes paid at each stage of the supply chain are not double-taxed. Businesses can deduct the tax they pay on purchases from the tax they collect on sales. This system promotes efficiency, prevents tax cascading, and encourages compliance. ITC is a fundamental feature in many value-added tax (VAT) and goods and services tax (GST) systems worldwide, facilitating smoother functioning of the tax regime and reducing the burden on businesses.

With an input tax credit, you can pay the remaining amount and deduct the tax you have already paid on inputs when paying output taxes.

Here’s how to do it:

You are responsible for paying taxes on purchases made from registered dealers of goods and services. The tax is collected when you sell. The amount of output tax, or tax on sales, is deducted from the taxes paid at the time of purchase, and the remaining tax liability, or tax on sales less tax on purchase, must be paid to the government. We refer to this method as input tax credit utilization.

A person registered under GST may only claim ITC if ALL the requirements are met.

ITC is only eligible for claims made for commercial use. ITC won’t be offered for products or services that are only utilized for:

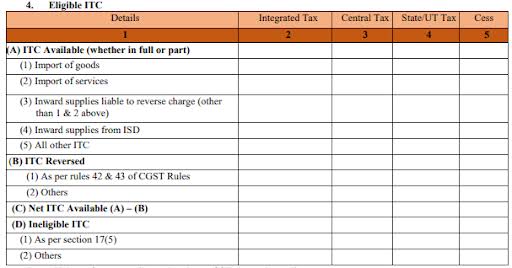

The input tax credit (ITC) amount is required to be reported by all regular taxpayers on Form GSTR-3B, their monthly GST reports. The summary figure of the eligible, ineligible, and reversed ITC for the tax period must be entered in Table 4.

Up to October 9, 2019, a taxpayer was eligible to claim any amount of provisional ITC. Later, the government imposed the following restrictions on the temporary ITC:

The following documents are required for claiming ITC:

In conclusion, Input Tax Credit (ITC) stands as a pivotal component in modern taxation frameworks, fostering economic efficiency, reducing tax cascading, and promoting compliance. By allowing businesses to offset taxes paid on inputs against taxes owed on outputs, ITC streamlines the tax process, ensuring fairness and accuracy.

Its implementation not only benefits businesses by reducing tax burdens and improving cash flow but also contributes to a more transparent and equitable tax system overall. As a cornerstone of value-added tax (VAT) and goods and services tax (GST) regimes worldwide, ITC plays a vital role in driving economic growth and facilitating smooth business operations.

Don’t miss our future updates! Get Subscribed Today!

Your trusted partner in business registration and compliance